Back in March, the pandemic caused massive fluctuations in the stock market and created one of the fastest unemployment spikes in history. Against that grim backdrop, many people decided to claim their Social Security benefits early. Now, some think tanks are estimating that the influx of new Social Security claimants, in addition to the reduced income from fewer people working, will cause the Social Security system to run out of funds even faster than projected – rather than 2035 as the last Social Security Trustees report indicated, it could be as early as 2029.

If the Social Security system were going broke, it makes a lot of sense to just claim early. However, the “claim early because Social Security is running out of money” argument is often dramatically oversimplified and can cause people to claim out of fear.

If this year’s recession were to be similar in scope to the Great Recession of 2008-2009, roughly 69% of benefits will be paid based on the current revenues after 2029. The most recent Social Security Trustee’s report suggested that 79% of benefits would be paid after 2035, without accounting for the pandemic and resulting economic impacts. Regardless of the estimate, it’s a far cry from stating that Social Security will simply disappear. A more accurate statement would be, “changes are coming.”

What's Been Done to Solidify the Social Security System in the Past?

In 1983 the Social Security system was out of money and on the brink of collapse. A variety of changes were implemented at the last minute to fix the system. Two changes that can be considered "benefit cuts" were the introduction of taxation on Social Security benefits and changes to full retirement age. Prior to the amendments, Social Security benefits were tax-free. After the amendments, up to 50% of a Social Security benefit could be taxable as ordinary income. The change to taxation effectively reduced take-home Social Security benefits for higher income people, but did not change the mechanics of when to claim.

Full retirement age was changed from age 65 to age 67 and phased in over 40 years with a key focus on preserving the "fairness" of the system. Those who were born in 1960 or later receive their full $1,500 benefit at age 67. If they claim as early as possible, at age 62, they only receive 70% of their Social Security benefit. The check will be smaller than if the full retirement age was 65—which means the change in full retirement age was essentially a "benefit cut." But even with the change, it is still advantageous to claim late. This particular benefit cut did not change how you would make the decision about when to claim. It only changed the net total.

Part of the 1983 amendments was the creation of an actuarily fair delayed retirement credit, increasing the credit from 3% to 8% per year for delay past full retirement age. Inevitably any cuts to the system will likely also be accompanied by changes that enhance benefits for some beneficiaries. In order to create a viable plan today given a huge variety of potential changes it makes sense to look at a bad case where the trust fund is fully exhausted.

Case Study: A Bad Case, No Compromise

Let’s take a closer look at the impact of potential benefit cuts. Your client, Roberta, is a healthy female who will turn 62 years old this year. She has a $2,000 monthly benefit at her full retirement age of 66 and 8 months. Claiming at age 62 would get her $1,433 per month. Claiming at age 70 would get her $2,533 per month. That’s a 76% increase for delaying. If we have a high level of confidence that full benefits will be paid, especially in this current low interest rate environment, then delaying is the best decision for most people.

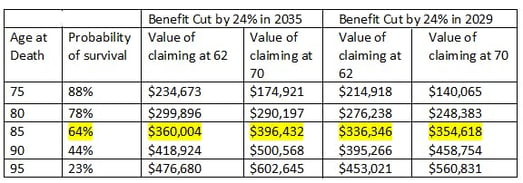

If Roberta claims at 62, under an assumption that benefits will be cut by 24% in 2029, then she will receive full benefits for nine years from 2020-2029, at which point her check would be cut by about $344 per month. If she delays, she will only get one year of full checks, at which point her cut will be $607. That may seem like a pretty negative outcome, but when we project the impact out over Roberta’s lifetime, the impact is still not enough to suggest that most people should claim early. Below is a table of the lifetime value of Social Security benefits based on various ages of death.

Lifetime value of Social Security benefits based on various ages of death.

The first column is Roberta’s age at death. The second column is her probability* of reaching that age. The following columns outline the cumulative value of benefits to those ages. The figures are presented in present value, which means that they account for the fact that if you claim early, you could invest the funds**.

*Survival probabilities based on longevityillustrator.org for a 62-year-old, non-smoking female in average health

**Real discount rate of 0.4%.

A female in average health who is 62 today has a 64% chance of living to age 85. Regardless of the benefit cut scenario that could be experienced, you’ll notice that by age 85, she would be better off by delaying benefits. When her risk of outliving her other assets grows, the benefit continues to grow, such that it is over $100,000 (in today’s dollars) by the time she reaches age 95, and she has a 23% chance of reaching that age!

On-Demand Webinar

Looking for more information about Social Security benefit cuts? This free on-demand webinar will take a closer look at the future of Social Security and show you how to craft good claiming strategies in the face of potential benefit cuts. You will learn:

- Why Social Security will continue to be an important retirement income stream

- How claiming early can leave a lasting negative impact for many of your clients

- How you can optimize your clients' Social Security claiming strategies

- How to alleviate client concerns and communicate the value of a good Social Security claiming strategy

Watch the Accounting for Potential Benefit Cuts When Crafting Social Security Claiming Strategies webinar now.

Millions of retirees rely on income from Social Security, and it’s understandable that recent events have left many nervous about their future plans. Benefit cuts would change longevity considerations a little bit, but it does not support the idea that everyone should claim early.

See the Impact

Our free Social Security benefit cuts calculator helps you show clients how benefit cuts could affect their retirement strategy. Simply plug in year of birth, benefit amount at FRA, percentage of benefit cut, and the year the benefit cut occurs, and instantly see the impact.

.svg)