Now that we're facing a market downturn, it's more important than ever to make sure your clients are on the right track to make the most of their retirement income and avoid paying more taxes than they need to. Your retired clients are relying on you to help them make their funds last through these uncertain times. Here are a few specific considerations for preparing retirement income strategies for clients this year.

>>>Start a 10-day free trial of Tax Clarity.<<<

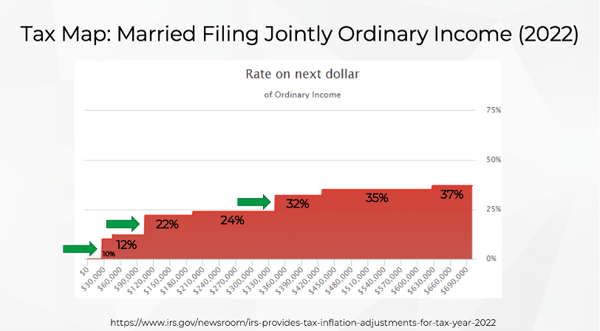

Maximize the Tax Bracket

Take advantage of everything you can at the 0% bracket, fill the 12% bracket, or avoid the next Medicare premium surcharge. Each of these points represents a big increase in taxes due. If your client is sitting in the middle of the 12% bracket, they may want to get more money from an IRA at the 12% bracket. This strategy can keep money from landing in the 24% tax bracket or higher later in retirement. That's the idea behind maximizing the bracket when planning retirement income.

Social Security Taxation

A good portion of your clients will have taxable Social Security income since they have multiple sources of retirement income. First, determine how much will be taxable . Take half of the Social Security benefit plus ordinary income, dividends, and capital gains. Then add in non-taxable interest. This is the client's provisional income. Then apply the income thresholds to the provisional income. Fifty cents of every dollar exceeding the first threshold becomes taxable as ordinary income. If you exceed the second threshold, 85 cents of every dollar over becomes taxable as ordinary income until you reach the maximum taxable amount (85% of the total Social Security benefit).

Blending Income Sources

Blending different income sources can help clients minimize the impact of taxes during retirement, specifically when reviewing the concentration of Social Security income versus IRA withdrawals.

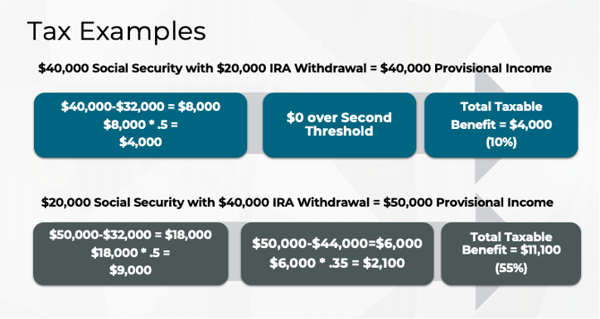

For example, to calculate taxable Social Security for a married couple filing jointly with $40,000 in Social Security benefits and $20,000 in IRA withdrawals, you add half the Social Security benefits ($20,000) to the IRA withdrawal. That equals $40,000 of provisional income. This couple is $8,000 over the first threshold ($32,000 for married couples) for total taxable Social Security of $4,000. In this case, they have $60,000 of household income, and only 10% of their Social Security benefit is treated as taxable income.

If you flip the figures, so the couple has $20,000 in Social Security benefits and $40,000 in IRA withdrawals, you get a very different result. Add half the Social Security benefits ($10,000) to the IRA withdrawal, and you get $50,000 of provisional income. Since the clients have $18,000 over the first threshold, they will pay $9,000 in taxes. Fifty cents on the dollar are taxable over the first threshold, and they are $6,000 over the second threshold ($44,000 for married couples). So, in this case, the total taxable benefit is $11,100 out of $20,000 or 55% of their Social Security benefit. MORE THAN HALF THEIR BENEFIT IS TAXABLE.

Medicare Premium Surcharges

While Medicare premium surcharges aren't technically considered a tax, you still need to be aware of their impact on a retirement income strategy. Unlike the exclusion of Social Security benefits for ordinary income tax, the retiree’s full Social Security benefit is included. If the client falls even one dollar over a threshold, they will need to pay an extra Medicare Part B and Part D premium. Premiums are based on income from two years ago, so it’s worth paying attention to the thresholds as you consider how much to take from various accounts.

Taxable Capital Gains

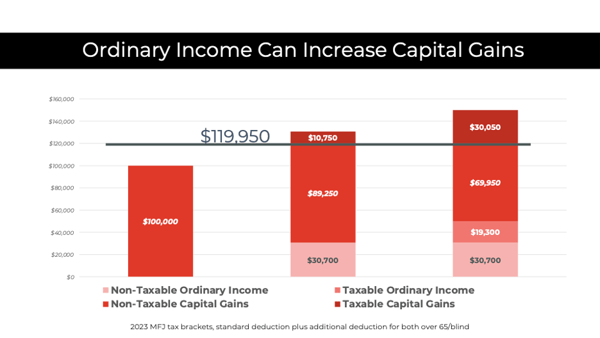

There are often situations where capital gains become taxable based on interactions with other retirement income. A married couple over 65 can have up to $89,250 of capital gains and pay zero federal income tax. For instance, if they have $100,000 in capital gains alone, the capital gains would be completely tax-free. However, suppose the clients have $100,000 in capital gains and a $28,000 IRA withdrawal. In that case, the standard deduction will wipe out the IRA withdrawal and push some of the capital gains out of a 0% capital gains bracket and up into a 15% capital gains bracket. So even though the ordinary income didn't create any tax on ordinary income, it created some capital gains tax.

Effective Marginal Tax Rates

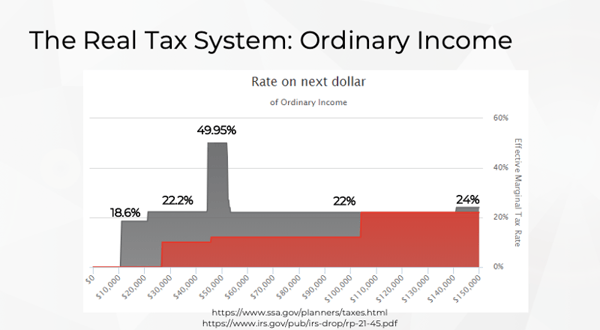

It's not the tax bracket that matters most in retirement income tax planning, but the effective marginal tax rate. How much does the client lose to taxes on the next dollar they withdraw?

Let's say your clients are a 65-year-old married couple filing jointly with $61,000 of combined Social Security and one of them delayed collecting their benefits. They have $10,000 in net long-term capital gains and $52,000 in IRA withdrawals. Once they have more than $10,000 in IRA withdrawals, they experience an 18.5% effective marginal rate. That is the point that their ordinary income plus capital gain drags enough Social Security into the calculation to begin making every additional dollar withdrawn from the IRA taxable at 10% and each additional dollar over that drags another 85 cents of Social Security into the mix, creating an effective marginal rate of 18.5%. This couple never really experiences the 10% or 12% brackets. They go from 18.5% to 22.2% to almost 50% before dropping down to back into the regular brackets.

The surprise for many is that they may lose 50 cents on the dollar on a portion of their retirement income to federal income tax. In this example, the couple falls in the 12% tax bracket, so they pay $120 of ordinary income tax, but the additional $1,000 withdrawal moves $850 of Social Security into the taxable range adding an additional $102 in taxes. Which causes $1,850 of capital gains to move out of a 0% capital gains bracket and up into a 15% capital gains bracket for a total of $277.50. When you add the additional taxes on that IRA withdrawal you get $499.50, an almost 50% effective marginal rate on a $1,000 withdrawal.

Tax Challenges and Opportunities During a Market Decline

When the market declines, advisors can provide tactical opportunities to resolve tax challenges, by tax loss harvesting. Using those capital losses to offset gains can help you reduce a concentrated, low-basis position, or rebalance to a more appropriate model, which can either solve the risk problem or an asset location problem. Be aware of wash sale rules when considering this strategy.

Loss harvesting can be an effective tax strategy during a down market. However, in many situations, you only want to harvest losses if there is a point where you can use those losses to offset gains. The Tax Map in Tax Clarity® can help you identify situations where this strategy may be effective.

Sometimes a client buys an alternate position they intend to hold for 30 days, but the market turns around. They may want to get out of the alternate position and back to the core asset allocation as soon as possible after the 30 days since the primary position is presumably the better investment path for the long term. However, you could recognize short-term capital gains if there is a massive asset class runup. Effectively you can end up trading out long-term capital gains for short-term capital gains. Trading out preferred rates for ordinary income rates is a challenging position. So be mindful of that 30-day window as you determine if it makes sense to recognize any short-term capital gains to rebalance those alternate positions.

>Watch the Retirement Tax Strategies During an Economic Downturn webinar on-demand.<

Tax Clarity

Tax Clarity® can help you take advantage of these tax strategies and more. Demonstrate tax opportunities and help clients avoid pitfalls. Run alternative scenarios and compare them to the original case side-by-side. Tax Clarity is ideal for financial advisors who want to take their services one step further and show how taxes will influence any retirement strategy. Check out this software demonstration.

.svg)