New Legislation Offers Significant Retirement Income Planning Changes

The Setting Every Community Up for Retirement Enhancement Act or the SECURE Act was signed into law last week, and the new legislation offers significant retirement income planning changes. For advisors who specialize in retirement income planning, particularly for the mass-affluent, the legislation includes three major changes to review.

1. Required Minimum Distributions

The first is the change to required minimum distributions (RMDs). RMDs will begin at age 72 rather than age 70 ½. What does that mean for advisors? It will be simpler to explain because we'll be working with round numbers and the "half birthday" is not relevant going forward. Second, it opens up the potential for an additional couple of years of Roth conversions in order to bring down those eventual RMDs. Keep in mind that anyone who reached 70 ½ in 2019 or prior stays on the old rules. Managing RMDs has always been a big focus in Income InSight® with the alternate harvesting patterns that you're able to choose from. However, the importance is going to be greater and the willingness of the community to listen to those sorts of techniques is always greater in times of change.

2. IRA Contribution Age Caps

The second major change is the ability for anyone who is currently employed to contribute to an IRA. IRA contributions are no longer capped by age. So, if you’re 74 years old, and you have earned income on your return (or your spouse has earned income), you'll be eligible to contribute to a traditional IRA. Of course, traditional IRAs were the only retirement savings vehicle that had that limitation in the past.

There will be a couple of opportunities for clients who are employed part time now that they don't have required minimum distributions until age 72. For example, they have a little bit of earned income coming in, but maybe they're living mostly off non-qualified investments. If that's the case, oftentimes you might have the ability to make an IRA contribution and qualify for a savers credit. Those clients can often look poor on paper, which may qualify them for that thousand dollar tax credit. That's a change that's going to impact some portion of your clients.

3. Stretch IRA Limits

The third change is probably the most significant big-picture change for retirement income planners, and that is the change to stretch IRAs. The stretch IRA has now been limited to 10 years. If your client inherits an IRA and the death of the original account owner occurs after 2020, that money is going to have to come out within 10 years. You can do it all in any one year along that 10-year track. Sometimes you may want to lump it into a few years. Other times you may want to stretch it out over a 10-year period. However, at 10 years, it all has to be gone.

This change also impacts Roth IRAs. While Roth IRAs have always been an incredible legacy vehicle, the fact that the stretch IRA is capped on the traditional IRA side will make Roths more attractive, because if a Roth is inherited, it's not going to bump a higher income beneficiary into an even higher tax bracket. For a lot of mass-affluent and lower-affluent individuals, we're going to find life insurance to actually be much more attractive relative to a Roth than it has been in the past because the distribution period for the Roth is also limited to 10 years.

We really want to look to the fact pattern of the client. If the client is a conservative-to-moderate investor who really was unlikely to be aggressively invested in the Roth anyway, they may also have other actual insurance needs, particularly the need for long-term care. So, when you have a situation where the Roth is not likely to dramatically outperform from an investment perspective and you have insurance needs that are well met by life insurance or long-term care riders on life insurance, I think you're going to find that life insurance actually stacks up a lot better post-SECURE act against a Roth IRA than it has in the past. We're going to see that evolve quite a bit as more and more software companies, like ours, update software to make that a really fair comparison and really understand the situations where a Roth is definitely better and situations where life insurance is definitely better.

Inside the SECURE Act: For Financial Advisors and Your Clients

To help you meet your clients’ changing needs and help you understand the changes brought about by the SECURE Act, we've created a free guide.

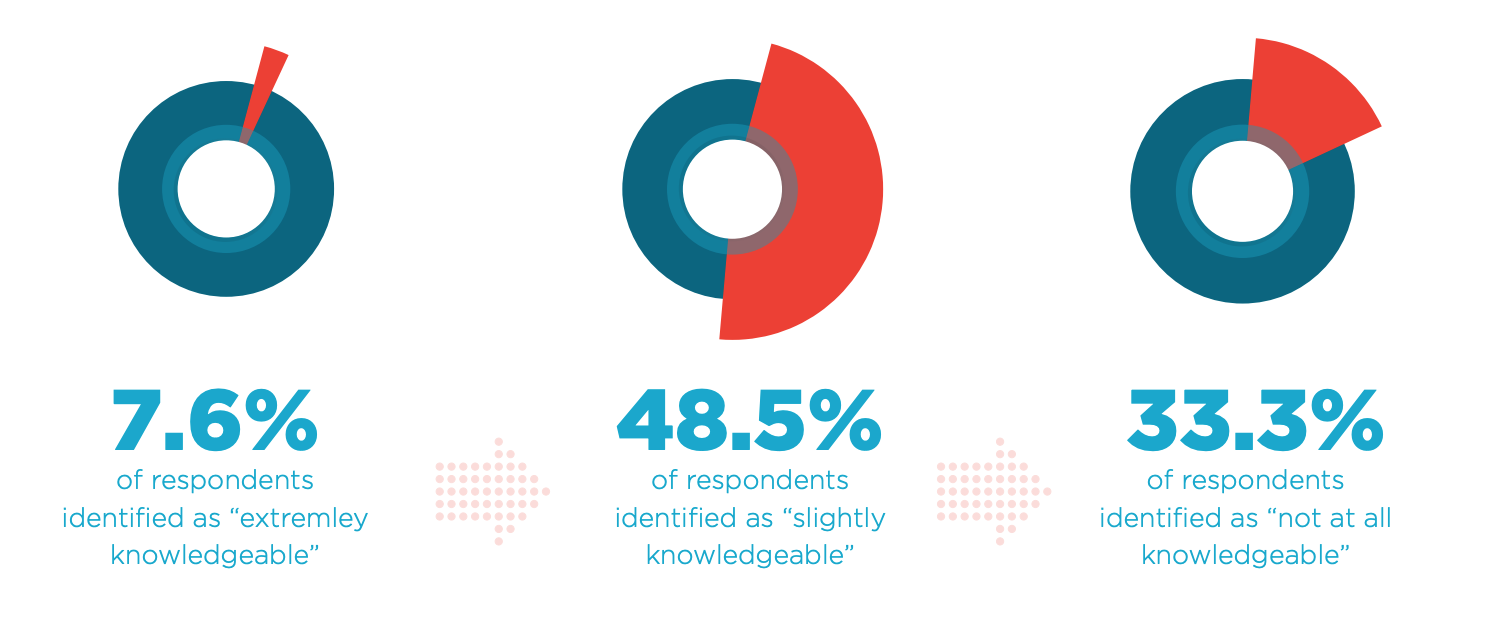

Our new guide outlines the most relevant changes for advisors who specialize in retirement income planning, particularly for the mass-affluent. The guide also includes survey results and feedback from Covisum contacts across the financial services industry. When asked about their knowledge of the new legislation,

- 7.6 percent of respondents identified as "extremely knowledgeable."

- 48.5 percent said they were only somewhat or "slightly knowledgeable."

- 1/3 of all respondents said they were "not at all knowledgeable."

It is worth noting that this lack of familiarity with the SECURE Act isn’t correlated to a lack of overall experience in financial advising. More than 86 percent of respondents have more than 10 years of experience in the wealth management field. Additionally, 48.5 percent of survey respondents said that more than half of their clients would be impacted by the SECURE Act.

It is worth noting that this lack of familiarity with the SECURE Act isn’t correlated to a lack of overall experience in financial advising. More than 86 percent of respondents have more than 10 years of experience in the wealth management field. Additionally, 48.5 percent of survey respondents said that more than half of their clients would be impacted by the SECURE Act.

“Today more than ever it is important to provide our community with education on these changes,” says Jose Sanchez of Retirement Wealth. “The net result of the unaware majority will be paying more in taxes and leaving less to the people they care about or the charities they love. I am providing monthly education classes that address the seven threats in retirement.”

Learn more about the changes brought about by the SECURE Act and how you can help clients navigate the new legislation. Download your free guide.

How Can Covisum Help Navigate the SECURE Act in Your Practice?

Significant changes in legislation can present enormous opportunities for the advisors who know how to capitalize. Income InSight can help you identify and project how expenses, income streams, accounts, investments, and insurance could be used throughout a client’s lifetime to supply the after-tax retirement lifestyle they desire.

.svg)