Social Security

Are Your Social Security Recommendations Influenced by Bias?

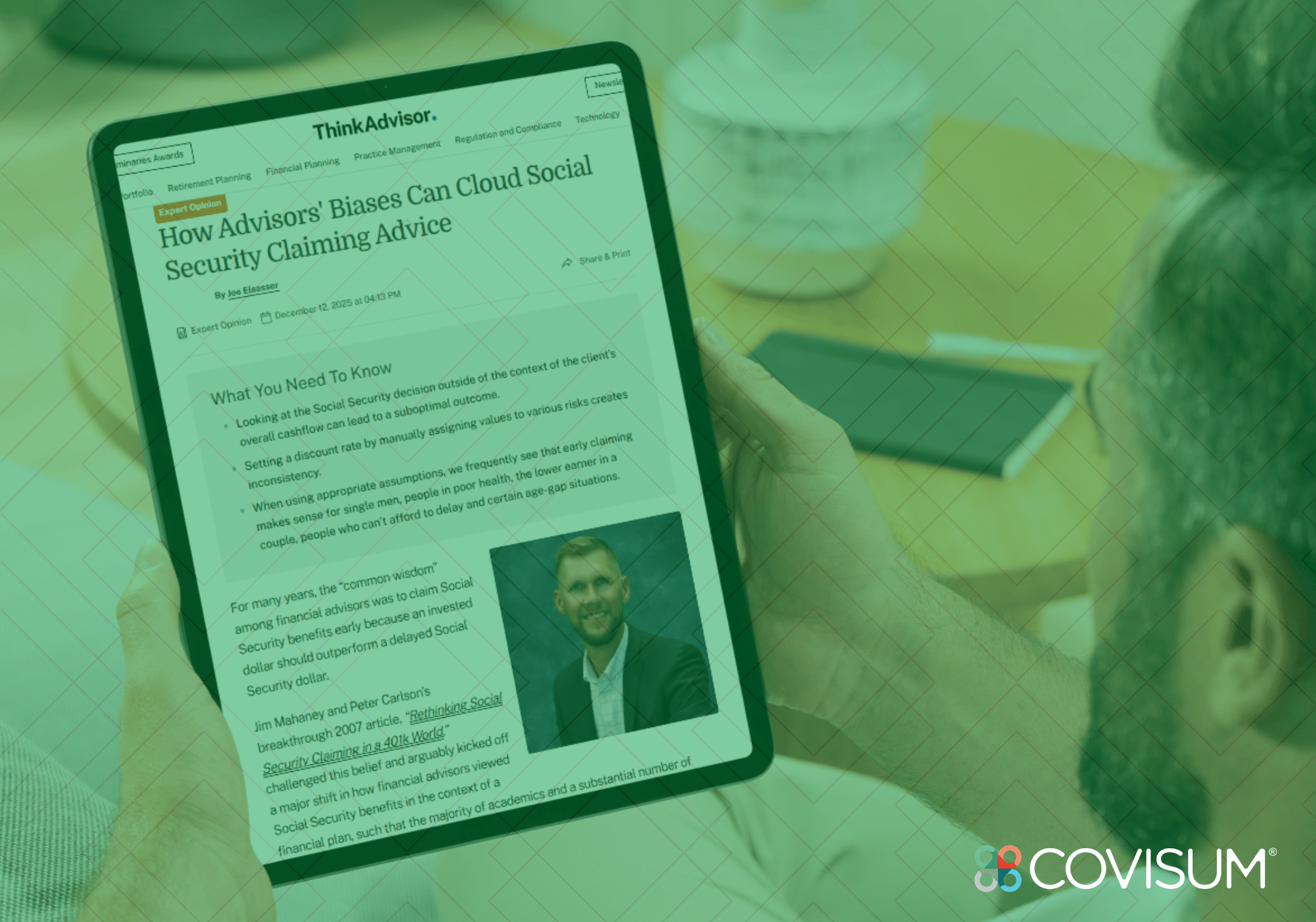

In a recent ThinkAdvisor article, Joe Elsasser discusses the biases advisors face when structuring processes around Social Security analysis. One key assumption is the selection of a discount rate - specifically whether we should discount future benefits by a conservative discount rate, or a more aggressive discount rate, such as the portfolio's rate of return. Advisors need to examine motivations for accepting or rejecting those arguments. Both narrow framing and rationalization biases may influence the decision framework.

Read

.svg)