Tech Processes in Practice

Thousands of advisors across the U.S. use one of Covisum's tools separately to offer actionable insights into individual elements of the financial strategies they produce. Each week, more and more advisors are stacking Covisum's individual tools to build better and more comprehensive retirement strategies that include: income withdrawal strategies, Social Security, tax efficiency, portfolio comparison and more. Read on to see how you can provide the big-picture perspective that differentiates you from other advisors.

This case study highlights one of the many ways you can use all four Covisum solutions to build a comprehensive retirement strategy and add value for your clients.

Case Study: Building a Retirement Investment Strategy

James Johnson and Jennifer Johnson are a married couple who have come to you for help with their retirement plan. They are a little uneasy when they walk into your office. They feel overwhelmed by all of the different details and considerations, and they don’t know who to trust. The right process can make them feel comfortable.

Start with Social Security Timing®

You know that Social Security should be the foundation of the overall retirement plan. For a married couple, it doesn’t always make sense for both individuals to simply delay their benefits; there are other factors to consider. For example, if James and Jennifer have debt and high interest rates or illiquid assets that can’t currently be used for retirement income, one spouse may need to claim early and one may need to wait since they may need the cash flow. Start by running a report in Social Security Timing® and reviewing the suggested alternate strategy. Social Security Timing allows you to see which claiming strategy will make the most sense for James and Jennifer.

Stress Test the Strategy

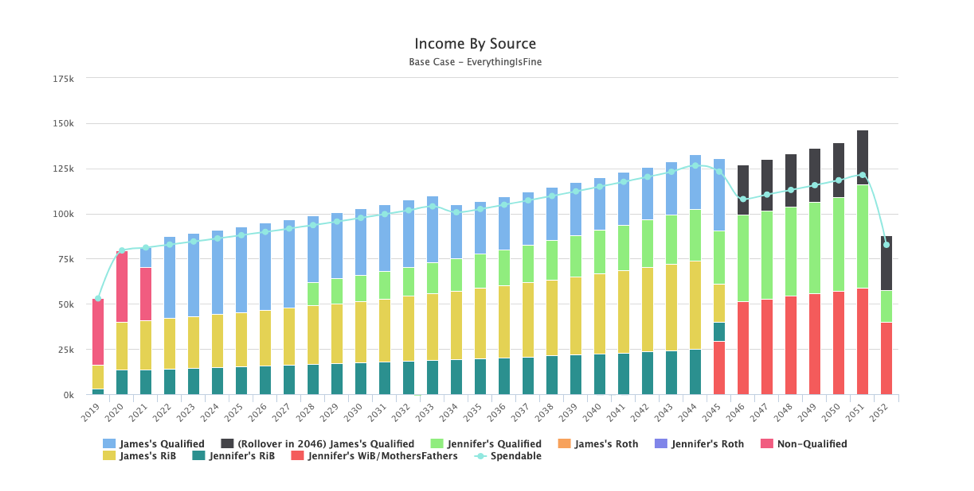

Jennifer and James mention that they have been eagerly awaiting retirement so they can spend more time with their grandchildren. Additionally, they plan to start traveling more, so their expenses will be higher early in retirement. You use Income InSight® to highlight the individual income streams year-by-year. The platform displays a color-coded graph with the various income streams sorted to make it easy for James and Jennifer to see the cash flow.

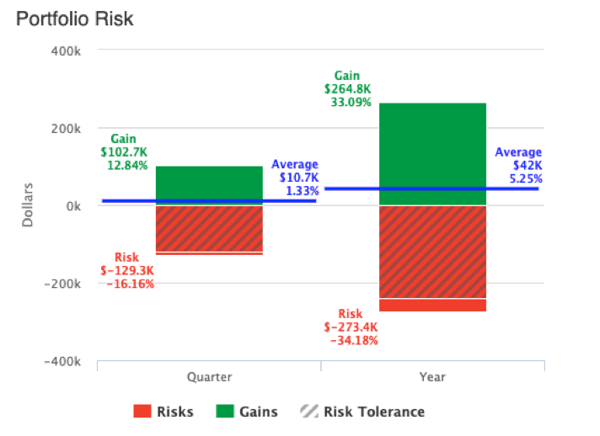

It also displays key retirement income metrics including portfolio longevity, sustainable income, and estate value. In this case, you can see that Jennifer and James need 33 years of retirement income, which their current path delivers in a good economic scenario.

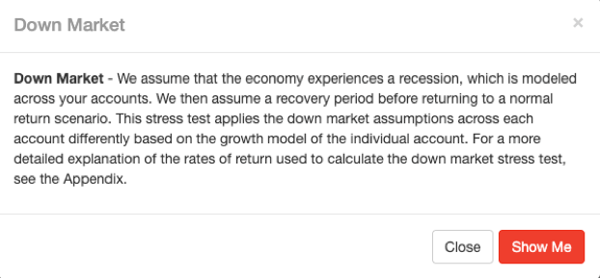

You also notice the down-market stress test icon is red, so you click on it to demonstrate the impact of a poor sequence of returns.

When you click “show me,” the case metrics update, and you can see that James and Jennifer’s retirement income would only last 20 years, and only 48 percent of their annual retirement income need would be met after depletion.

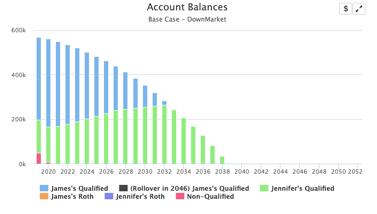

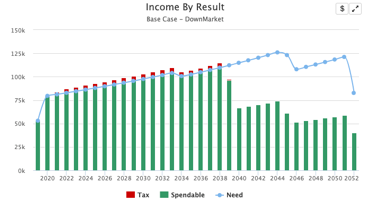

You may also want to review the account balances and income by result charts, as these demonstrate the impact visually.

Similar failures occur upon James’ untimely death or in the event either member of the couple needs long-term care. Clearly, there is some work for you to do.

Find an Opportunity for a Roth Conversion

Income InSight also creates a multi-year Tax Map, and you can take a closer look at the tax situation of any given year by using Tax Clarity®. Jennifer and James feel really good about their tax situation, but you recognize a potential opportunity with a Roth conversion. They will pay no federal income tax for the next two years while spending from their non-qualified account. In 2019, they could take about $23,000 more out of their IRA while still paying no federal income tax. They could take a similar amount in 2020.

Next, you take a closer look at their portfolio using SmartRisk®. Generally, James and Jennifer are pretty risk-averse, and you need to make some changes to bring them back to where they are more comfortable. Traditional financial planning software might address a portfolio failure by increasing risk across all client accounts. While this may improve the probably of success, it also likely magnifies the consequences of failure. Further, it may cause you to recommend a portfolio that the client is unlikely to maintain through a down market. You absolutely don’t want to give a client a portfolio that’s too aggressive for their “gut” and increase the likelihood of them selling in the middle of a dip, precluding their ability to experience a recovery.

Determine Risk Tolerance

Income InSight provides a check on James’ and Jennifer’s goals, in light of their portfolio, and accurately establishes their risk capacity, and SmartRisk helps you accurately determine their tolerance.

You use Income InSight, Social Security Timing, Tax Clarity, and SmartRisk to build a strategy to help James and Jennifer reach their goals. Here are a few techniques you use (any number of options could solve their challenges).

1. Portfolio Changes

-

James's Qualified reallocated to Moderate.

-

Jennifer's Qualified reallocated to Aggressive.

-

Non-Qualified reallocated to Conservative.

2. Refine Spending Strategy

-

Change amount for Travel Budget with a monthly amount of $350 from 1/1/2019 to 1/1/2034.

-

Change amount for Discretionary Income with a monthly amount of $750 from 1/1/2019 to second death.

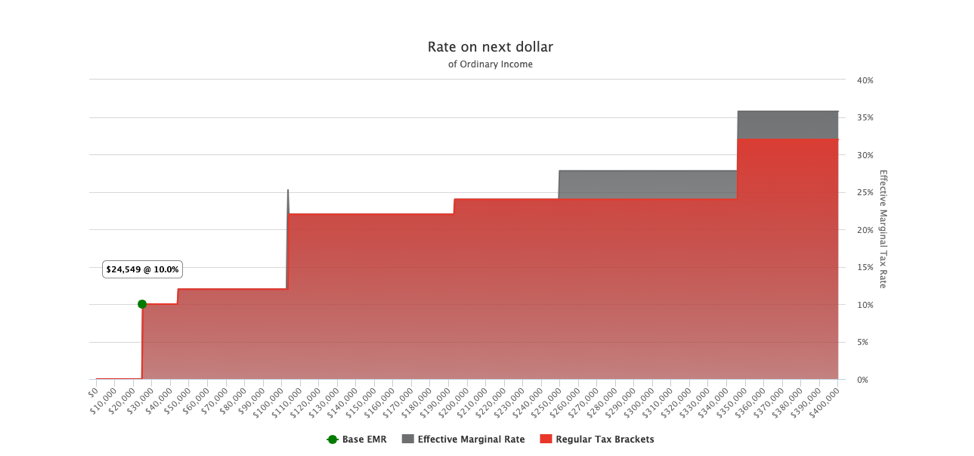

3. Utilize non-qualified funds for income needs and taxes while making annual conversions to a Roth IRA that would be taxed at a rate less than the average Effective Marginal Rate for your lifetime in the Base Case.

4. Implement the following Social Security Strategy

February 2025

-

James files a standard application for benefits requesting a month of election of May 2025 at 70. James' first check would be received in June 2025 for approximately $3,810.

May 2027

-

Jennifer files a standard application for benefits requesting a month of election of August 2027 at 70. Jennifer's first check would be received in September 2027 for approximately $2,357.

Build Your Custom Tech Stack

You have all of the tools to alleviate James’ and Jennifer’s concerns and make sure they feel prepared for the next chapter of their lives with a comprehensive retirement investment strategy. Show them what their retirement could look like with an overview in Income InSight or dive into specifics with Social Security Timing, Tax Clarity, and SmartRisk.

.svg)